Healthcare Research

Explanation of source links: Throughout the research below, you will find links of three types. The first and most frequent type is to primary sources such as governmental agencies. The second is to nonprofit groups that generally use government data or their own research to support their philanthropic mission. We have tried to use the least biased of these, or when in doubt, we have identified their bias. The third is to articles in periodicals or newspapers that we find to be of interest. These are not meant to be construed as original sources, and in some cases may not be accessible, depending on a reader's frequency of prior visits to the linked periodical or newspaper.

Important clarification of terms

The public healthcare discussion often confuses terms and morphs several questions that should be examined and debated separately.

The first question is about the quality of US healthcare: Is it better or worse than what is available in other countries?

The second question is about the cost of US healthcare: Is it priced fairly and similarly to the healthcare of other countries?

The third question is about administration and payment: Is the method of administration and payment an efficient one?

The Question of Quality: How does the US compare to other countries?

There are several common measurements used to compare the quality of healthcare across countries. Unfortunately, the US ranks toward the bottom in every single one of them. The relevant data are broadly available from multiple sources and not generally disputed. We have relied heavily on the Commonwealth Fund for this discussion. The Commonwealth Fund’s Multinational Comparison of Health Systems Data, last compiled in 2017, is particularly useful.

Measure One-Avoidable Mortality: This is defined as “Deaths Before Age 75 from Conditions that Are at Least Partially Modifiable with Effective Medical Care.” In the Commonwealth Fund study, the US ranked 19th on this measure, which is the worst of all of the developed countries surveyed.

Measure Two-Major Disease Survival Rate: The US measures poorly with respect to several diseases within this category. Again, in the Commonwealth Fund study of nine developed countries between 2001 and 2004, the US ranked seventh in asthma, meaning Americans “diagnosed with asthma die sooner than their counterparts in seven of the countries.” The same is true of diabetes, meaning that Americans with diabetes died younger than diabetics in all eight other countries.

Measure Three-Deaths Due to Surgical or Medical Mishaps: The Commonwealth Fund found that the US ranked poorly in this category. For example, Americans have the worst survival rate after kidney transplants.

Measure Four-Life Expectancy: According to OECD Data, the US ranks 26th amongst OECD countries, as follows:

SEE ALSO:

Measure Five-Infant Mortality: Also according to OECD data, the US ranks 29th in infant mortality.

Measure Six-Healthy Life Expectancy at Age Sixty: Since the US has a lower life expectancy at birth than other wealthy countries, analysts think it is helpful to examine how long someone at the age of 60 might expect to live well. Again, in a 2006 survey by the Commonwealth Fund, out of 23 countries, the US was tied for last.

Measure Seven-Access to Healthcare Services: When compared to the average of OECD countries, the US per capita has fewer physicians (2.4 versus 3.1), fewer nurses, and fewer hospital beds.

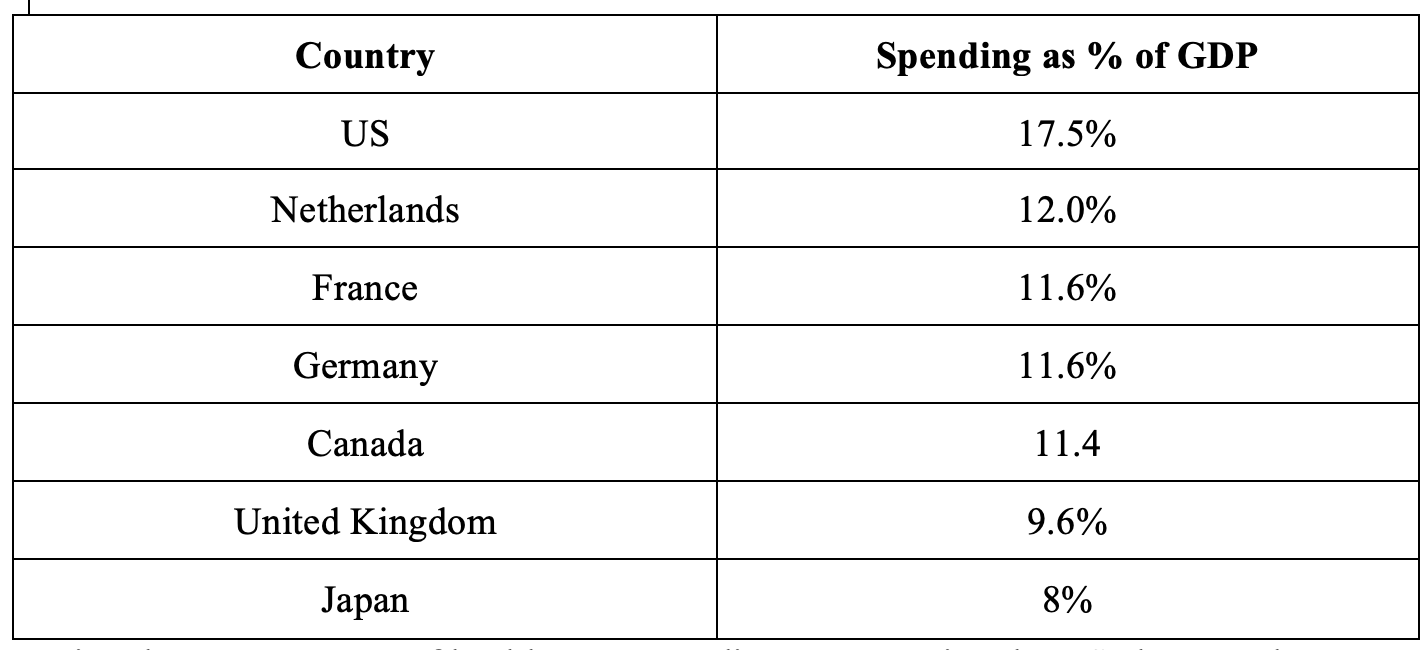

The Question of Cost: Is it true that the US spends more on healthcare than other developed countries?

Yes. The most common measurement of healthcare spending is total spending as a percentage of a country’s Gross Domestic Product (GDP). In this category, the US spends far more than other comparable countries, despite the fact that each of the countries compared below provides universal healthcare to all of its citizens.

Using the measurement of healthcare expenditures per capita, US also spends more than any other OECD country. The following comparison, as well as a host of other valuable data can be found in an article written by Bradley Sawyer and Cynthia Cox of the Kaiser Family Foundation entitled “How does health spending in the U.S. compare to other countries?”

The Peter G. Peterson Foundation provides a useful merger of these two concepts: spending versus outcomes in four different measurement categories. Again, the US spends more for less in each of them.

the Question of Administration and Payment: Is the US as efficient as comparable countries?

There are several reasons that the US spends more on healthcare compared to other countries, all of which we will discuss here. The largest of these categories, however, is the overall cost of healthcare administration and payment in the US. These costs can be broken down into two major categories:

Private insurance company delivery: Unlike most other developed countries, the US administers non-Medicare and Medicaid payments for healthcare through a system of private, for-profit health insurance companies. The insurance company has several responsibilities in this system: underwrite (meaning choose whom to insure and whom not to); review claims and determine which ones to pay and not to pay; negotiate prices with caregivers, hospitals, and drug companies; and make a profit. When you take all of this expense into consideration, the average insurance company pays out about 80% of the premium that it collects. This compares to 97% for Medicare, which is about the same for countries like Germany, France, etc.

Presence of complexity: In addition to the cost of insurance administration, the US payment system is relatively complex, given the presence of Medicare, Medicaid, the Veterans Administration, the myriad of private insurance companies with their own rules and processes, public service insurance, etc. Managing this complexity represents an enormous cost to individual physicians, hospital staffs, etc.

According to researchers from Harvard University and the London School of Economics such administrative costs added up to approximately 8% of GDP, compared to 3% of GDP in10 other developed countries.

This factor alone, therefore, is the largest driver of the cost of the US system.

To quote T.R. Reid in The Healing of America, “The administrative monstrosity we have built costs us a lot of money—by far the highest administrative costs of any health care system on earth. The U.S. Government Accountability Office concluded that if the country could get the administrative costs of its medical system down to the Canadian level, the money saved would be enough to pay for health care for all the Americans who are uninsured.”

Each of the following characteristics of our system contributes but in a smaller way.

Provider compensation: According to the same study referenced above, the US had higher provider healthcare compensation than the comparable 10 countries. Generalist compensation in the US was $218,173, compared to a range of $86,607 to $154,126 in the countries compared. Similar findings exist for the compensation of specialists and nurses.

Drug prices: Any number of studies demonstrate that drug prices in the US are higher than comparable countries, and that the US spends more per capita on prescription drugs than the same countries. In order to ensure that comparisons are accurate, studies also examine utilization. Here, the finding is that the US is not an outlier in the volume or type of drugs consumed. The primary driver, therefore is price. A common explanation for this is that the US relies on the competitive marketplace to control price, whereas other countries with single payers negotiate price at the national level. In the US, Congress specifically forbade Medicare from negotiating prices. As a result, the US consumer literally subsidizes the drug prices offered to the rest of the world.

Testing and prices for services: Comparison studies of the prices of services, tests, surgical procedures and hospital stays also find that prices are higher in the US than elsewhere. In their article “How do healthcare prices and use in the U.S. compare to other countries?” Rabah Kamal and Cynthia Cox of the Kaiser Family Foundation examine and illustrate this fact accross a few common procedures and services.

Litigation: Studies have also shown that the cost and frequency of medical malpractice litigation in the US are greater than in other comparable countries. As a result, doctors pay considerably more for malpractice insurance, expect to be sued multiple times during a career, and charge more for their services accordingly. Insurance costs for all consumers are higheras a result. A 2010 study conducted by the Harvard School of Public Health found that medical liability costs added 2.4% to total medical spending in the US. Finally, the US Department of Health and Human Services reports that “Americans spend far more per person on the costs of litigation than any other country in the world.”

Shortage of doctors and hospital beds: Although it cannot be proven that a smaller supply in these categories results in higher prices, we can observe that in the US, as noted above, there are fewer doctors and hospital beds per capita than in the comparable countries.

How is health Insurance purchased and paid for in the US?

As indicated above, private insurance companies are the primary method of administering non-government provided healthcare. As a result, the appropriate question is, “How is insurance purchased?” According to the research by the Kaiser Family Foundation found in “Key Facts about the Uninsured Population” published December 7, 2018, Americans obtain or fail to obtain insurance in the following ways:

49% of the public obtain health insurance through their employer. Generally individuals share the cost of the premium with their employer.

19% of Americans qualify, based on their state of poverty for Medicaid, which is essentially government-provided health insurance.

14% of Americans, due to having reached the age of 65, qualify for Medicare, also government-provided health insurance.

7% of Americans purchase their insurance privately, 2% of Americans are covered by the military or Veterans Administration, and 9% have no insurance.

What do we know about the 9% of Americans who have no healthcare coverage?

When surveyed, Americans without health insurance cite the following reasons: Cost is too high (45%), lost job or changed employers (22%), lost Medicaid (11%), employer does not offer coverage or employee is ineligible for coverage (9%), family status change (11%), or no need for health coverage (2%).

Also, we know that of those who do not have insurance, 13% are unemployed, 77% have at least one full-time worker in the family, and 10% have a part-time worker.

What are the consequences for those without health insurance?

First, Americans without health insurance obtain less preventive healthcare and, as a result, often incur greater costs in the long run.

Secondly, Americans without health insurance rely on emergency room visits for general healthcare, which is an expensive and inefficient way to provide care.

Thirdly, the same Kaiser Family Foundation study quoted above estimated that in 2015 one million adults declared bankruptcy as a result of outstanding medical bills. They also found that 26% of Americans between the ages of 18 and 64 struggled to pay medical bills. Accordingly, healthcare providers expend considerable effort collecting payment and managing write-offs, thereby raising the cost for all.

What is the history of healthcare reform efforts?

For several decades, policymakers and public officials have made efforts to make sure that every citizen has access to health care.

During the Great Depression, President Roosevelt was deeply concerned about the state of American healthcare. He hoped to include nationalized healthcare in the Social Security Act but retreated in the face of opposition from the American Medical Association.

During the Second World War, the government froze wages and prices to facilitate the war effort. Unable to compete for employees based on wages, employers began to offer health insurance as a benefit not subject to price controls. As employer-provided healthcare developed and healthcare costs increased, retirees were increasingly unable to afford healthcare following retirement. Those working in low-wage professions also struggled, as typically such employers did not provide coverage. As a result, President Johnson proposed and passed the Medicare and Medicaid programs in 1965 to provide coverage to retirees as well as those in low-paying professions.

Ever since, policymakers have struggled to standardize healthcare for US citizens. In 1971, Senator Kennedy proposed a form of universal healthcare. President Nixon also had proposals in process but these were derailed by Watergate. President Clinton tried again unsuccessfully in 1992. Finally, in 2010, President Obama passed the Affordable Care Act (ACA). As discussed below, however, the ACA did not provide for single-payer universal coverage and instead settled for expansion of access to Medicaid and private insurance.

What was the ACA and how did it work?

In America’s Bitter Pill, Steven Brill articulates the elements of the healthcare debate that resulted in the 2010 passing of the ACA. Brill says that generally, policymakers recognized two broad challenges in the US healthcare system: cost and access.

First, looking at cost, Americans pay considerably more than other countries. Secondly, a significant portion of Americans do not have access to healthcare for reasons that include cost, as well as pre-existing conditions and the loss of employer coverage. Policymakers also recognized a fundamental reality: that, at 18% of GDP, the US cannot afford to provide insurance to all Americans. If we can reduce the cost of healthcare to the level seen in other countries, however, we would be able to provide healthcare to all of our citizens just as other countries do. Policymakers recognized, therefore, that they had to focus on reducing the cost of healthcare. Standing in the way of cost reduction, however, was a host of special interests including the AMA, the insurance industry, the bar association, medical equipment manufacturers and pharmaceutical companies.

Concluding that significant progress on the cost front was unrealistic, the Obama administration settled for a complicated mix of small cost concessions from the major special interests, increasing taxes on individuals and equipment manufacturers, adding a pre-existing condition exclusion, creating a national exchange, and expanding Medicaid.

More specifically, the ACA successfully did the following:

Required individuals who don't receive health insurance benefits through their employers to purchase coverage or pay a penalty. The theory was that if everyone (including the relatively healthy) purchases insurance then the average cost for everyone will decline.

Created subsidies to help low-income families pay for the cost of their health insurance.

Implemented strict guidelines for what insurers are allowed to do with respect to eligibility and coverage:

Insurers cannot cancel policies when a policyholder becomes sick

Insurers can't place a lifetime monetary limit on any benefits deemed "essential" in new policies

Insurers can't deny coverage because of pre-existing conditions, or enforce higher premiums within the same age/geographical group because of gender or pre-existing conditions (besides tobacco use)

Created the Health Insurance Marketplace (HIM) which provides easier access to plans for both businesses and individuals

Expanded Medicaid eligibility to those earning 133% of the federal poverty level

Prohibited employers from making their employees wait more than 90 days for health insurance eligibility

Implemented a penalty of $2,000 per employee on employers who do not provide health insurance

For those who already had coverage before the ACA

Certain types of preventative care must be covered at no additional cost to the patient

Prohibited annual and lifetime dollar limits on care

What were the overall outcomes of the Affordable Care Act?

By the end of the 2016 enrollment period, 12.7 million Americans were covered under state and federal exchange plans and the percentage of uninsured Americans declined by about 5%. The result was a decreased probability of people not receiving necessary medical care by 20-25%, and an increase in the probability of people having a usual place of care between 47.1% and 86.5%.

While the ACA successfully expanded access to healthcare, however, it fell short in reducing cost. The primary reason for this was that major providers did not provide reasonable concessions. Another reason is that the minimum viable policy of the ACA was more expensive than policies people had access to prior to the ACA.

What is the current state of the ACA?

In July 2017, the Republican Party attempted but failed to repeal or repeal and replace the ACA. Since that time, they have passed a provision repealing the individual mandate—which will inevitably weaken the overall program.

In addition, President Trump signed an executive order asking federal agencies to make new rules for cheaper, bare-bones health plans. He has also reduced (where possible) government subsidies known as “cost-sharing reductions.” These reductions reimburse insurers for discounts they give to policyholders with incomes under 250% of the federal poverty line (or about $30,000 in income a year for an individual). These discounts shield lower-income customers from out-of-pocket expenses such as deductibles or copayments. These subsidies have been the subject of a lawsuit that is ongoing.

The Trump administration’s impact on the ACA also includes: Eliminating the Small Business Health Options Program (SHOP) marketplace, shifting responsibility to the states to offer provider networks and access to community providers, elimination of agreed upon compensation to insurers for subsidized individuals, and action by the Department of Justice to legally invalidate the pre-existing condition exclusion.

What is the mix of private versus public funding in the US versus other countries?

Another way to look at healthcare spending in the US is to review how the mix of public and private spending compares to other countries. According to the same Kaiser Family Foundation article referenced above, public healthcare spending in the US is 8.5% of GDP, which is roughly equal to that in Germany, the UK, France, Belgium, Austria, Canada and Switzerland. The difference is that public spending in each of these cases enables coverage for all citizens. In effect, the private sector in the US makes up for the amount by which US total healthcare spending exceeds that of comparable countries.

What does healthcare look like in some of the countries setting an example for affordable and accessible healthcare?

France: The World Health Organization has called France’s healthcare system the world’s No. 1 system. France ranks at the top for almost every one of the healthcare outcomes mentioned previously, and achieves this result despite the fact that they provide healthcare to every resident–or perhaps because of it. Contrary to public perception in the US, the French see a doctor an average of eight times per year, compared to five per year for Americans. They also consume more medication.

Several aspects of the French healthcare system are similar to the US system. Healthcare is provided by a system of private doctors, and a mix of private and public hospitals. Those who are employed obtain their insurance from their employer and contribute to the cost. The comparisons, however, stop there.

In France, there are very few insurance plans, and they each depend on your region and occupation. Every insurance plan is defined by the government. If you lose your job, your coverage continues and the government pays the employer’s share. You cannot be excluded for pre-existing conditions. Prices of services are set, drug prices are negotiated, and patients know exactly what they will pay before they receive the service. As a result, providers make less than they do in the US and hospitals run more efficiently and at lower cost. Patient information is contained in a single electronic system such that no manual record keeping is required and every provider knows at all times what a patient’s history is. Billing is automatically handled through the national healthcare card at the end of the appointment. Payments are administered through nonprofit “insurance entities” whose costs are minimal inasmuch as they do not have to underwrite, review claims, or make a profit.

The result of all this is that France spends less than 10% of GDP (versus 18% in the US) and still provides healthcare to every citizen. Their spending per capita is half that of the US despite the fact that every resident is covered.

Germany: Germany also has one of the best healthcare systems in the world when measured by the standard comparisons. Their approach is similar to that of France with similar results: Germany spends 11% of GDP on healthcare (versus 18% in the US).

Like France, Germany controls the price of healthcare services and drug prices. Provider compensation is therefore lower than in the US. They distribute insurance through employers with employees and employers sharing the cost. In contrast to France, where there are only a handful of plans, Germans have nearly 250 different plans to choose from. The plans are provided by nonprofit “insurance companies” called “sickness funds” that compete for business. Any German can choose any one of the plans regardless of their employer and can keep the plan when they change jobs (or change it at any time). Sickness funds cover all Germans unless you meet a certain wealth level, in which case you can opt for the private market. Again, the government pays the premium in the event that a citizen can’t afford it. The cost of administration is very low (approximately ⅓ the cost of administration in the US).

Japan: Japan is another example of a country that provides excellent outcomes at very low cost. The Japanese spend only 8% of their GDP on healthcare, and yet they are at the top of charts in terms of outcomes and have nearly twice as many doctor visits per capita per year as the US. There are no waiting lines and no rationing, as is commonly charged.

As in Germany and France, most Japanese healthcare is administered through private providers. Their costs, however, are tightly controlled by the government. Payment administration is provided through one of 3,500 “insurance plans.” You do not choose your plan; rather, it is assigned to you depending on your employment status. Large companies are required to provide insurance at their own cost; small companies do so with subsidies; and the government also subsidizes the self-employed, unemployed, and elderly. In each of these cases, individuals pay a reasonable share of the total cost with certain maximums. The purchase of insurance is mandatory, and there is no exclusion for preexisting conditions. Companies must pay every claim that is submitted.

For our specific healthcare recommendation, please click here.